A promissory note can be a very useful item to know how to write. Promissory note samples might give you a rough estimate of what you need to include in this kind of note, but you will probably still need more information on hand to write a good note for your use. When you need to write a promissory note for payment, you want to be sure that all the right information is in the note so that it can be useful later on.

A promissory note is a document that sets out all the details of a loan that has been made between two parties. The two parties need to abide by the details of the loan itself while the loan exists, and the promissory note guides this process. Small loans might only need a simple promissory note to be protected, but you should still create this document when the loan is granted.

Table of Contents

- 1 Promissory Note Templates

- 2 What does a promissory note do?

- 3 Can I write my own promissory note?

- 4 Promissory Note Forms

- 5 How do you write a promissory note?

- 6 Promissory Note Samples

- 7 Do promissory notes need to be notarized?

- 8 How do you secure a promissory note?

- 9 Promissory Note Examples

- 10 Some other information that you might need to add to your note

- 11 FREE Promissory Note

- 12 Promissory Notes Are Critical for Some Loan Processes

Promissory Note Templates

By State

What does a promissory note do?

Both a secured promissory note and an unsecured promissory note are made to help outline the details of the relationship between a borrower and a lender. This document makes sure that the borrower fulfills their promise to pay back the lender before the end date of the loan. There is typically a specified timeframe that is allowed for the repayment process to be completed, and this is part of what the promissory note outlines.

The promissory note can also be used to prove that the loan exists and that both parties are in agreement about the fact that money changed hands and a loan was granted. In simple situations, the promissory note might take the place of a formal loan arrangement. If the payment period is only going to be a few months, this might be all that is needed to handle a very small loan.

Can I write my own promissory note?

Yes, there is no reason that you cannot write your own promissory note. There are some common reasons that you might need to create one of these documents. The typical situations where a promissory note might be needed are:

- Student loans

- Bank loans of various kinds

- Car loans

- Personal loans of any amount between family members or friends

There are also some other names that the promissory note can go by. These alternate names do not impact the use of the note itself, and they do not change the legality of the document in any way. You can call your promissory note by any of these other names and still expect that it will function as a promise for repayment:

- Debt Note

- Demand Note

- Commercial Paper

- Notes Payable

Your state or your area might use one of these names in place of a promissory note. In these cases, the most common term for the note itself can be used for the sake of clarity.

Promissory Note Forms

How do you write a promissory note?

Promissory note examples are written much the same way if they are for secured purchases or for unsecured purchases. You will need to be sure that you have the right information in the document to ensure that it can be related to the loan in question and used to verify that the debt will be paid back by the end of the loan period. The more detailed the promissory note, the more useful it will be if it needs to be used to secure payment or to take collateral that the note was secured with.

- Full Names of the Parties Involved in the Loan. The borrower and the lender will need to be identified by full legal name. You will also want to be sure that each of the parties is listed with their address and phone number. The identification of these parties needs to be done properly, or the promissory note will not be valid. Nicknames are not acceptable in this part of the document.

If the lender is a company or business, the full legal business name will need to be listed as well. If there are more than two people receiving the loan, they will both need to be indicated on the loan alongside one another.

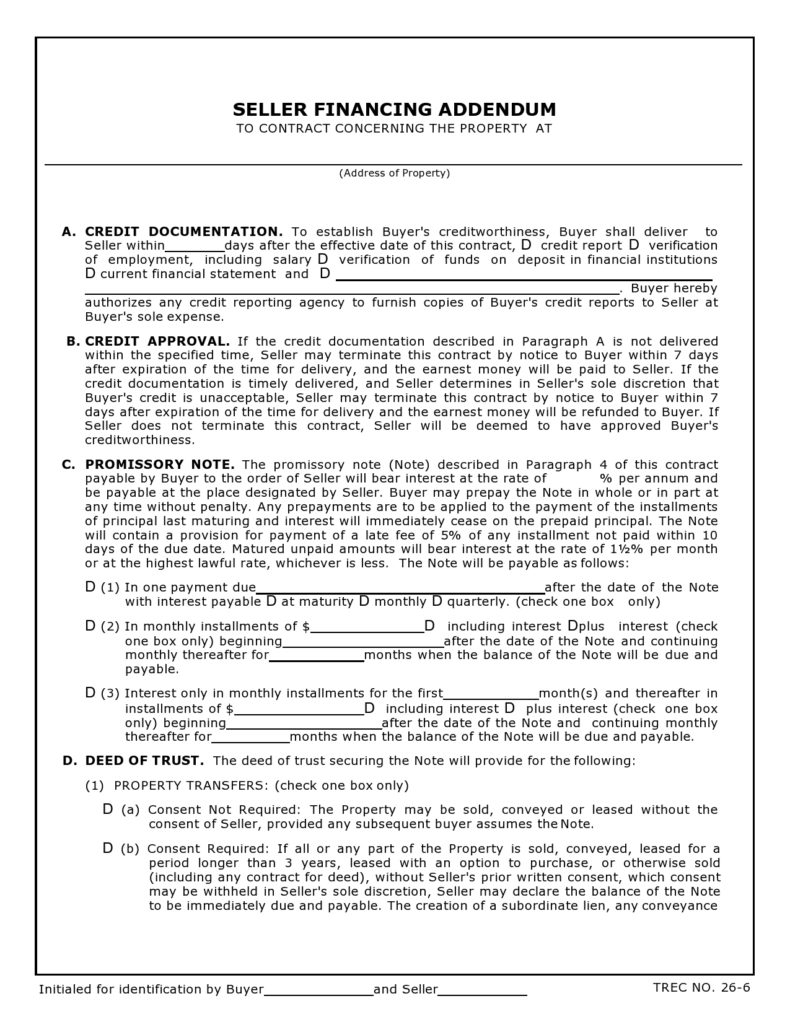

The lender can be listed as the “payee”, the “issuer”, or the “maker”. The borrower can also be called the “payer” or the “buyer”. These terms need to be used consistently when the parties are not indicated by name later in the document. Make sure that whichever term you decide to use, you do not change it out for another term later in the document. - Repayment Amount. The repayment amount is the most important part of the information that needs to be listed in the promissory note. This is the total amount of the loan amount, including interest and fees, and charges that are related to the loan. The lender might or might not charge interest, and the total loan amount needs to indicate the correct total in either case.

There are various ways that interest might be charged, and lenders who do so for a living will probably charge a standard interest based on a fee schedule that is related to risk-based pricing. Private loans can have whatever interest assessed that the lender and borrower decide is fair. State laws might restrict the amount of interest that can be charged on a loan as well.

In places like California, for example, the maximum interest that can be charged for a loan is 10%. Florida, however, allows for an interest rate of up to 18% for amounts less than $500,000. It is always wise to check the amount of interest that can be charged for your promissory loan per state laws. - Payment Plan. There are various ways that payments can be made on this kind of loan. Lenders will often have very limited options that are offered to those who take out a loan. However, private loans can be more flexible in the payment options that are offered.

Installment payments are the most common payment style for this kind of loan. The payments are made on a schedule that allows for the original payments to go more toward interest with a shift toward payments to the principal throughout the life of the loan. Installments might also be paired with a balloon payment as the final step in the repayment process. This is not as common as regular installment payments.

You might also elect to use a lump sum payment model or a payment-on-demand model. These are also viable options for your promissory note but are less common since the loan will be paid off nearly right away without an installment payment plan. - Consequences of Non-Payment. Default on the loan can lead to collections actions being taken against the person who took out the loan. There are state limitations on the collection process that need to be considered when you write this part of the document. The lender can usually take back the collateral on the loan if the loan is a secured loan as part of the repayment process when there is a default related to payment.

Legal action can also be taken against the borrower when the promissory note and the loan are defaulted on. This legal action can vary from state to state, so you will need to check on these details before you can write this part of the document. - Notary. If you decide that you want to notarize your promissory note, you can elect to do so. State laws can impact this part of the document’s requirements as well. This is not typically required, but it can help to give the document more legal weight if it is felt that this step needs to be taken.

- Signatures. As with the loan documents related to the promissory note, the lender and borrower will need to sign the document and date the signature lines. An unsigned promissory note is legally useless, so make sure that you get this part of the document taken care of.

Promissory Note Samples

Do promissory notes need to be notarized?

As stated above, you do not have to have your promissory note notarized. However, this can give the document more legal weight and can make it more useful if you need to enact collection actions against someone who has defaulted on their loan.

How do you secure a promissory note?

Promissory notes are typically secured with collateral of some kind. This might be the item that the loan is for, such as a car, or the collateral for the loan can be something of value that the borrower owns outright. This might be a home, jewelry, or something else of value. Securing a note is important so that the promise to repay the loan can be enforced if necessary.

Securing a loan with collateral is common in the loan industry for just this reason, and a promissory note can be secured in the same way. The collateral that is being used to secure the loan should be clearly stated in the promissory note so that the lender has the right to take the collateral if the loan is not repaid.

Promissory Note Examples

Some other information that you might need to add to your note

If you have never written a promissory note, you might want to know some of these other terms as well. These terms can come in handy in certain sections of your note when it comes to clarifying the specifics of the agreement between the lender and the borrower.

- Acceleration: This clause can be added to your document if you wish to allow for immediate repayment if the borrower goes bankrupt, fails to make payments, or passes away. There might also need to be this kind of clause if the borrower wants to pay off the note early or runs into other financial difficulties.

- Amendment: Changes to the agreement should be required to be done in writing and agreed upon by both parties. It is always a best practice to be sure that no changes are allowed without discussion and a written alteration to the original document.

- Joint and Several Liability: This clause states that co-borrowers will also have a responsibility to pay for the debt individually as well as collectively.

- Governing Laws: State laws might apply to your promissory note, and you can indicate which ones are here in this section of the document.

- Collateral: The details of the collateral that is being used to secure the loan will often need to be given in the document. If the loan is unsecured, this section can be left out.

- Right to Transfer: This clause indicates if the party who took out the loan can transfer the promissory note to another party.

- Prepayment: This part of the document will state if the borrower can pay off the debt early without penalty. This impacts the interest that is collected on the loan, and it is sometimes not allowed.

FREE Promissory Note

Promissory Notes Are Critical for Some Loan Processes

A promissory note can be a big benefit if you are worried about the repayment of a loan. You will be able to use the promissory note to govern repayment, to make sure that you can take the collateral that the loan is secured with, or to help establish a payment plan that the borrower can stick to. This is one of the key documents that can be used to secure a loan and make sure that both parties are on the same page about the lending agreement.

Promissory notes are not that difficult to write, and they can be so useful that they are worth your effort to learn to craft them. This is one of the best ways to be sure that you can secure a loan’s repayment. The more clear that everyone involved in the loan process is about the details of the agreement, the more likely it will be that the loan will be repaid.