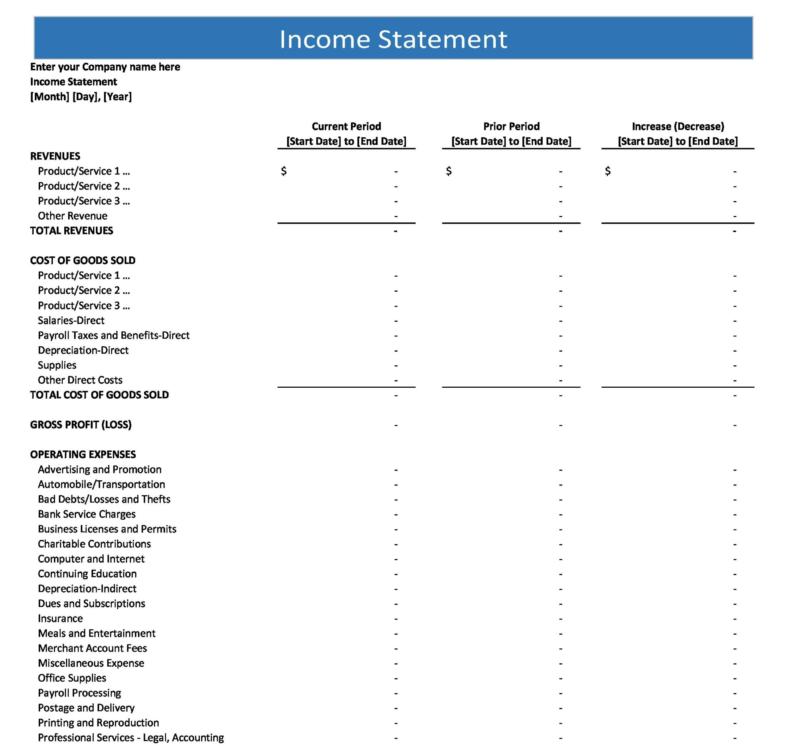

A profit and loss statement template, sometimes referred to as a P&L template or income statement, is a financial report that lists a company’s costs, income, and profits for a given period.

A sample profit and loss statement demonstrates a company’s ability to make money, drive sales, and control costs. These templates are created based on the principles of accounting. Some basic principles include the recognition of revenue, accruals, and matching.

Table of Contents

- 1 Profit and Loss Statement Templates

- 2 What Is a Profit and Loss Template?

- 3 What is Included in a Profit and Loss Statement Template?

- 4 Profit and Loss Statement Forms

- 5 The Components of a Profit and Loss Template are Broken into Three Main Categories:

- 6 Different P&L (Profit and Loss) Statement Types

- 7 Why is it important to have profit and loss (P&L) statements?

- 8 Profit and Loss Statement Examples

- 9 When to Use a Profit and Loss Template

- 10 How to Create a Profit and Loss Statement Template

- 11 Profit and Loss Statement Samples

- 12 Are P&L statements mandatory for all businesses to prepare?

- 13 Conclusion

A free profit and loss statement template and other financial records like balance sheets and cash flow statements make it easier to track finances accurately and predict future business performance.

Profit and Loss Statement Templates

What Is a Profit and Loss Template?

The P&L or income statement displays account changes over a predetermined time, just like the cash flow statement.

P&L starts with a revenue entry, or top line, and deducts business expenses such as the cost of goods sold, operating expenses, tax charges, and interest expenses.

P&L statements are also known as the following:

- Loss and profit statement

- Operation statement

- Financial performance or results statement

- Income statement

- Expense report

- Income declaration

What is Included in a Profit and Loss Statement Template?

Although P&L templates might differ amongst companies, most have the following essential elements:

- Company Name: Located at the top of the document, this is where your registered company name goes.

- Reporting period: The time allocated for the P&L statement (weekly, monthly, quarterly, annually, etc.).

- Sources of business income: (such as sales, dividends, interest, etc.) together with the corresponding dollar amounts.

- Gross income: This includes specified gross monthly income in detail.

- Cost of goods: Costs for labor and materials are included in this figure, but indirect costs like those for sales and distribution are not.

- Gross Profit: Verifies monthly profit, which is equal to your gross revenue minus COGS.

- Expenses: This is where your salary and benefits, rent or a mortgage, utilities, office supplies, etc. are itemized.

- Total Expenses: To determine total expenses, itemized costs should all be added up.

- Net Income: To get your net income, deduct all of your costs from your gross profit.

The following extra elements are also included in specific, more complex profit loss statement templates:

- Reductions: Includes any lower cost of products sold linked to inventory (e.g., shipping, handling, insurance, vehicle expenses, etc.), lower sales returns, or lower sales discounts.

- Net Sales: Calculated by subtracting any discounts, allowances, or returns from your gross sales total to determine net sales.

- Cost of Sales: Summary of all expenses incurred from selling your goods or services.

- Tax Rate: Indicate the percentage of earned income your company is taxed on.

- Taxes: To calculate your net income after taxes, itemize all your tax-related expenses.

Also, note that operational expenses can be calculated by aggregating all expenses, and operating income can be calculated by subtracting gross profit from total costs.

Profit and Loss Statement Forms

The Components of a Profit and Loss Template are Broken into Three Main Categories:

Expenses

Expenses are a breakdown of how much your business spent during a period. It includes all expenses related to maintaining your firm. Several instances include:

- Payroll

- Bank feed and interest

- Rent and utility charges

- Insurance

- Equipment

- Software

- Marketing initiatives

Revenue

Revenue, which is determined by multiplying the average sales price by the number of units sold, is the money made through regular business activities. It is the top-line amount from which businesses calculate net income by deducting costs.

Some of the methods of calculating revenue are:

- Total units sold multiplied by the average price.

- Total consumer’s average selling price per unit.

- Net revenue, which is the gross revenue minus adjustments, is another type of revenue. This type involves refunds, returns, discounts, or commissions.

Net profit

Net profit is when all costs are subtracted from revenue. It serves as the gold standard to determine profitability. It is also called the bottom line because it is found at the bottom of all financial statements.

All expenditures incurred to operate the business, including employees, rent, utilities, taxes, and other charges, are included in total expenses. This includes all income from sales, services, and other sources.

Even if this isn’t the only financial information that can be used to assess your company’s performance, it can also be useful in identifying what is and isn’t profitable.

To make your statement more effective, you need to add specific categories when designing your profit and loss statement format. These groups include:

- Revenue or Sales

- Net income

- Operating income

- Cost of sales, or cost of goods sold

- SG&A, also known as selling, general and administrative

- Marketing and advertising

- Tax deductible expense

- Taxes

- Technology

Different P&L (Profit and Loss) Statement Types

A P&L statement can be created in one of two ways. The cash method and the accrual method.

Cash

Only when cash enters and exits the business is the cash method, also known as the cash accounting method, used. This reasonably straightforward system tracks money that has been paid or received.

When money is received in a transaction, it is recorded as income; when it is spent on obligations, it is recorded as a liability. Smaller businesses and consumers who want to manage their money often employ this technique.

- Revenue is recorded under cash accounting once the customer makes a cash payment to the business for the goods or services received.

- Like sales, cash accounting only registers expenses once a cash outflow happens, which means the corporation has already paid the third party in cash.

- For a small business or private enterprise, P&L figures made using cash-basis accounting are more typical.

Accrual approach

With an accrual approach, revenue and costs are recorded in the period in which they occur rather than when cash is paid or received.

This approach employs double-entry accounting and aligns revenues with the costs incurred to earn them. Based on the matching principle, accrual accounting gives a more realistic picture of a company’s income and expenses.

This indicates that a business utilizing the accrual technique records the amount of money it anticipates receiving in the future.

For instance, even when it has yet to receive payment, a business that delivers a good or service to a customer, would record the anticipated revenue on its P&L statement. Similar to assets, liabilities are recorded even if no expenses have been paid by the business.

- Revenue is recognized by the revenue recognition principle when it is “earned” according to GAAP (i.e., when a product or service is supplied to the customer regardless of whether a monetary payment was made).

- The matching principle states that expenses must occur in the same period as the corresponding revenue they contributed to.

- According to U.S. GAAP guidelines, a P&L statement is mandatory when submitting using accrual accounting.

Why is it important to have profit and loss (P&L) statements?

The profit and loss statement’s goal is to display a company’s earnings and expenses for a given time period. You can also:

- Use P&L to Estimate Profitability

By integrating this data with insights from the other two financial statements, investors and analysts can use this information to evaluate the profitability of the business.

By comparing a company’s net income (as indicated on the P&L) to its percentage of shareholder equity (as shown on the balance sheet), an investor, for instance, could determine its return on equity (ROE). - Use P&L Templates to Track Statements from Different Periods

Comparing income statements from various accounting periods is crucial. This is because revenue trends, operational expenses, spending on research and development (R&D), and net income are more important than the raw figures.

For instance, a business’s revenues can increase steadily while its expenses might increase considerably faster.

Investors might assess a firm’s financial health further by comparing its P&L statement to that of another similar-sized company in the same industry.

Doing so can show that one company manages expenses more effectively and has a higher potential for growth than the others.

Profit and Loss Statement Examples

When to Use a Profit and Loss Template

A crucial component of any organization is developing a profit and loss template. Depending on when you need to produce them, you can create different types of templates, including:

- Periodic

Every business must occasionally create a sample profit and loss statement for its evaluation. As a result, you’ll need to produce such a declaration at least once every three months. The preparation of a business tax return and decision-making for firms are both aided by reviewing this statement.

When calculating net income to determine how much income tax your business should pay, a business tax return is another financial record that draws on data from the profit and loss template. - Pro Forma

New firms must develop unique profit and loss statements during the startup period. The term “pro forma” refers to a sort of document projected into the future.

Businesses might also require this kind of declaration when planning a new project as part of a funding application.

How to Create a Profit and Loss Statement Template

Even if your company doesn’t need initial capital from a lending institution like a bank, you still need a number of financial documents that can guide your decision-making. The profit and loss statement is undoubtedly one of the most crucial financial statements to produce.

The majority of the information for this statement would come from the first year’s cash flow statement or monthly budget for your business.

The data can also come from calculations of projected depreciation that you could get from a tax counselor. You specifically need the following:

- The company’s transaction listing, which includes a list of every transaction made on the checking account and every purchase made using a company credit card.

- Any other cash transaction for which you have the receipts, including petty cash transactions.

- A list of all the revenue sources for your business, such as credit card payments, checks, and so on. Bank statements contain all of this information.

You can produce unique P&L templates with Word, Excel, PowerPoint, Google Docs, or Google Sheets. Be sure to include all cash transactions, including income and expenses.

You might still need to manually input certain cash transactions, including those for income and petty cash if you utilize accounting software. Be sure to use an invoice or a cash transaction form each time a customer hands you cash.

Be sure to keep each receipt for any monetary payments. This is crucial for business-related travel and dining expenses.

Whatever kind of statement you require, the procedure for preparing for and acquiring the data needed to generate it is the same. Here are some actions to take:

- Show the sales or net income for each quarter of the fiscal year for your company first. To display the revenue for your firm from the many sources, you can divide the income into subcategories.

- List all of your company’s expenses for at least three months. Show a sales percentage for each of these costs. Verify that the sum of all of these costs equals 100% of the revenues.

- Earnings display the difference between expenses and sales. Earnings before interest, taxes, depreciation, and amortization, or EBITDA, is another name for this stage.

- Subtract EBITDA from the total interest paid on your company’s commercial debt for the fiscal year.

- Make a list of the projected taxes to be deducted from net income.

- Finally, display and deduct the entire fiscal year’s amortization and depreciation.

Financing banks could ask you to produce a statement that extends beyond the estimates by a year or two to demonstrate your company’s break-even point or the moment at which it begins generating consistent positive cash flow. The steps are as follows:

- Make a list of all potential costs. Overestimating the values and including a “miscellaneous” category is preferable.

- Create projections for the monthly sales of your business. Underestimate the times and values this time.

Profit and Loss Statement Samples

Are P&L statements mandatory for all businesses to prepare?

P&L statements and financial statements must be prepared by publicly traded corporations and filed with the U.S. Securities and Exchange Commission (SEC) so that investors, analysts, and regulators can review them.

When preparing these statements, businesses must adhere to a set of regulations and standards known as generally accepted accounting principles (GAAP).

Contrarily, private businesses are not always obligated to adhere to GAAP. However, some smaller businesses might still need to create formal financial statements.

Conclusion

Profit and loss statements demonstrate a company’s ability to be successful. Not only are these documents important for records and tax purposes, but they also serve as a foresight for future business performance.

Creating your profit and loss statement template can be an efficient way to ensure your company stays ahead of its competitors by staying on top of business performance rituals.